GCC Insurance Industry Poised To Grow In Post-Pandemic Era

- Insurance Featured News Regional

Global Business Magazine

Global Business Magazine- 7 minutes read

Overcoming the hurdles caused by COVID-19 pandemic, the GCC Insurance market is set to grow at the rate of 3.2% from $26.5 billion in 2021 to $31.1 billion in 2026.

Sustained increase in population, economic recovery, reopening of the tourism sector, and strong pipeline of infrastructure development projects are among the leading factors that will facilitate growth in the sector.

On the other hand, the life insurance gross written premium (GWP) is projected to grow at a compound annual growth rate (CAGR) of 3.8% from US$ 3.8 billion in 2021 to US$ 4.6 billion in 2026.

Within the region, the UAE remains the largest market and will continue to maintain its leading position as the insurance hub of the GCC. The insurance business is expected to reach $14.4 billion by 2026, in view of the rapid recovery of the Emirates’ economy, with a CAGR of 4.1% from 2021.

UAE Biggest Market

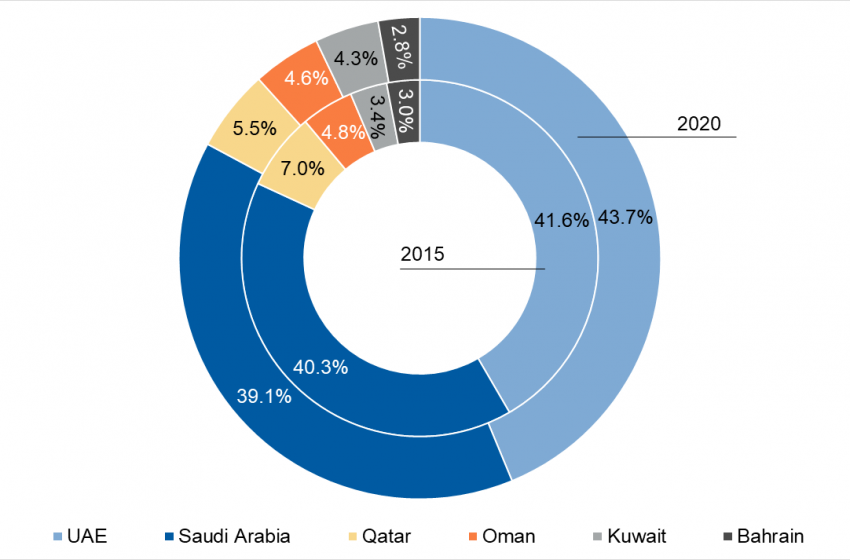

The UAE and Saudi Arabia retained their position as the two largest insurance markets, accounting for 43.7% and 39.1% of the region’s GWP in 2020, respectively. The UAE maintained its position as the leading insurance market, growing at a CAGR of 2.8% between 2015 and 2020,

Despite the challenges, the outlook for premium growth remains resilient, with regional insurers now focusing on developing new business models and introducing innovative products, while reimagining services and pricing strategies for priority segments.

These dynamics, backed by government initiatives to improve compliance in order to ensure sustainability, will enable the insurance industry in the GCC to emerge from the crisis.

These were the findings of a report released by Dubai-based Alpen Capital, which offers investment banking advisory services to institutional and corporate clients in the GCC region.

Coming to insurance penetration, the UAE (3.2%) and Bahrain (2.1%) registered the highest penetration rates. Penetration rate in the rest of the GCC nations ranged between 1.0% and 1.9% in 2020.

GWP in the GCC life insurance segment rose at an annualized rate of 1.7% since 2015 to reach $3.6 billion in 2020-21. The segment, which has been historically driven by the expatriate population base across the GCC, witnessed slowdown in 2019 and 2020 due to COVID-19.

Although UAE accounted for the largest share in life insurance market, constituting 77.3% of the total GCC life insurance GWP in 2020, it recorded a modest rise of 1.7% CAGR during the period.

Back To Business

Alpen Capital’s Managing Director (Corporate Affairs) Sameena Ahmed said that the growth of the GCC Insurance industry slowed down due to pandemic but has started recovering due to a rebound in the region’s economy.

“Moreover, reopening of the tourism sector and mega events such as the Expo 2020 and the FIFA World Cup 2022 are likely to provide additional boost to growth going forward,” she said.

“The pandemic has brought a shift in consumer behaviours leading to demand for innovative, customised and convenient solutions. This is likely to compel insurance firms in the region to either develop in-house technological capabilities or collaborate with InsurTech companies that can deliver improved customer experience,” Sameena Ahmed added.

On the other hand, the non-life insurance segment in the GCC is estimated to grow at a CAGR of 3.1per cent from $22.7 billion in 2021 to $26.5 billion in 2026. Sustained increase in population, economic recovery, reopening of the tourism sector, and strong pipeline of infrastructure development projects are among the leading factors that will facilitate growth in the sector.

M&A Activities

M&A activities across the GCC insurance sector remained buoyant during 2020, amid downturn in activities due to the COVID-19 pandemic.

The report said 2021 witnessed some revival in businesses as economies reopened, leading to the M&A activities stirring up again in the region. There were 9 M&A deals recorded in the GCC insurance sector, at par with the total number of deals recorded in 2019 and 2020.

The deals during the last two years comprised of a handful of cross-border and several intra-regional acquisitions as companies are looking to form stronger entities to offset weak profitability.

The region witnessed 18 intra-regional deals between 2019 and 2021, while there was just one deal wherein an overseas insurer acquired stakes in local companies to further establish its services in the market.

“Going forward, focus is likely to be directed towards value creating opportunities with larger players targeting small to mid-sized players as well as tech-enabled operators and aggregators. This will not only strengthen the competitive capabilities of the players in the market but also encourage the creation of newer products and services in the sector amidst weakening profitability,” said Krishna Dhanak, Managing Director at Alpen Capital.

Similarly, regional players made a strategic investment in a Germany-based foreign company to diversify their geographical presence. Going forward, focus is likely to be directed towards value creating opportunities with larger players targeting small to mid-sized players as well as tech-enabled operators and aggregators.

This will not only strengthen the competitive capabilities of the players in the market but also encourage the creation of newer products and services in the sector amidst weakening profitability.

The M&A activities across the GCC insurance sector remained buoyant during 2020, amid downturn in activities due to the Covid-19 pandemic. As economies reopened, 2021 witnessed some revival in businesses leading to M&A activities stirring up again in the region, the report added.