Traders work at Frankfurt’s stock exchange in Frankfurt, Germany, February 6, 2018. Picture taken with a fisheye lens. REUTERS/Ralph Orlowski

Morning Bid: It gets real

- Finance News World

Global Business Magazine

Global Business Magazine- 5 minutes read

A look at the day ahead in markets from Sujata Rao

Minutes from the European Central Bank’s February meeting are due later on Thursday but last month’s shock hawkish pivot seems like distant history now.

With Brent crude up some $30 a barrel since mid-February and European gas prices more than doubling in this period, the ECB will be looking with alarm at spiralling inflation expectations; Ten-year German ‘breakevens’, which reflect future inflation, have jumped 40 basis points since that February ECB meeting .

Shorter-dated breakevens are above 4%.

And while estimates vary widely of how the war will impact euro zone GDP, a growth hit is certain and that’s dampening the likelihood of near-term policy tightening.

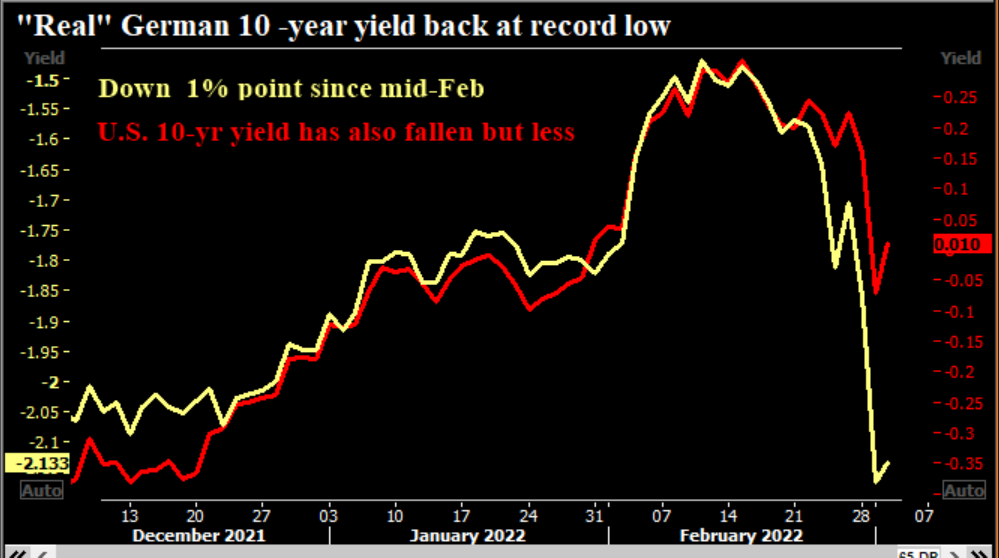

With markets paring expectations of an ECB rate rise this year, swathes of the regional bond market are back into negative-yield territory. Moves are more pronounced in “real” yields – borrowing costs after stripping out inflation — German 10-year real yields are at record lows below -2%.

U.S. Treasury real yields recovered a touch on Wednesday after Federal Reserve Chairman Jerome Powell clearly signalled a quarter-point rate rise was on the cards at the Fed’s March 15-16 meeting. (Though ten-year real yields around -0.9% are still half where they were earlier this month).

Stock markets are reflecting this transatlantic divide, and Citi advise clients to add exposure to U.S. stocks, in particular the tech sector which benefits from falling real yields. But they also remain positive on commodity-heavy UK stocks.

European stocks are opening weaker, despite a strong Wall Street close following Powell’s clear signal that a 50 bps rate rise is unlikely.

The bad news continues to pour in on the Russia front. Societe Generale acknowledged an 18.6 billion-euro exposure to the country. It’s further bad news for European banking stocks, already down more than 20% since mid-February read more .

Key developments that should provide more direction to markets on Thursday:

Japan’s service sector activity contracts at fastest pace in 21 months read more

China’s Feb services activity expands at slowest rate in six months read more

-Euro zone PPI/unemployment rate

-Emerging market central banks: Malaysia, Ukraine

-European earnings: Taylor Wimpey, Lufthansa, Thales, LSEG, ITV, Admiral, Fortum, Raiffeisen, Merck,

-U.S. earnings: Best Buy, Kroger, Costco, Gap, Marvell

Reporting by Sujata Rao;

This article was originally published by Reuters.